Eigenpie's airdrop gameplay, mechanism, prospects and revenue expectations

- WBOYWBOYWBOYWBOYWBOYWBOYWBOYWBOYWBOYWBOYWBOYWBOYWBforward

- 2024-02-04 10:25:071114browse

php Editor Apple will introduce to you the airdrop gameplay, mechanism, prospects and revenue expectations of Eigenpie in this article. Eigenpie is a new cryptocurrency project based on blockchain technology, and its airdrop mechanism has attracted the attention of many investors. Through airdrops, projects can issue free Eigenpie tokens to users holding specific tokens, thereby promoting community building and user participation. This article will analyze Eigenpie’s airdrop gameplay and mechanism in detail, discuss its future development prospects, and provide some suggestions and analysis on revenue expectations. Let’s take a deeper look at Eigenpie’s airdrop-related content!

This Thread will analyze Eigenpie’s airdrop gameplay, mechanism, prospects, and revenue expectations to help you clearly maximize your returns.

A. Airdrop gameplay

Currently deposit stETH and wait for LST to enter to get triple benefits:

Eigenpie Points , an airdrop corresponding to 10% of the total amount;

Eigenlayer points (after Eigenlayer opens deposits on February 5);

Eigenpie corresponding to the total amount 24% IDO share, 3M FDV low valuation;

Basic return on deposited LST (for example, if mETH APR is 7%, you can continue to enjoy 7%);

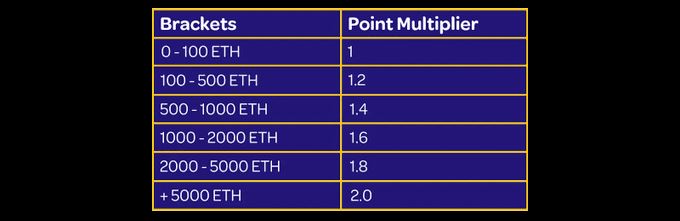

Points will provide gains based on the total size of the team. The larger the team, the greater the increase, up to twice as much, so it is best to stay together for warmth.

B. Mechanism

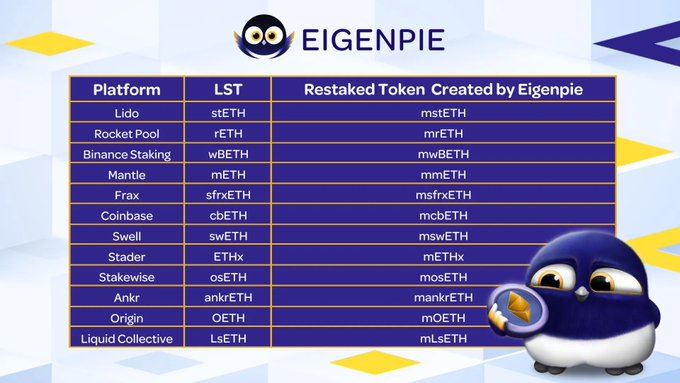

What Eigenpie does is isolate LRT (ILRT). Each LST sends a corresponding Token to isolate risks, see the table below:

Eigenlayer currently has so many LSTs on it. If an LRT project accepts it in general, then this project will bear the risks of all underlying LSTs. Once a certain LST has a security problem, it may It will cause a devastating blow to it.

So there is Eigenpie’s ILRT to isolate the risk.

Isolate risks and isolate liquidity. Will this cause problems? In fact, it doesn’t matter. Compared with LRT that supports Native Staking, one of the advantages of LRT that supports LST is that it can fully utilize the liquidity of the underlying LST. Individual pairs such as mrETH/rETH and mmETH/mETH are actually more conducive to cooperating with LST project parties to stimulate liquidity.

C. Prospects

What are the advantages of this project? After all, it was indeed released a little late, but there is indeed a gap in demand that has not yet been filled: LSTs who have joined Eigenlayer are eager to participate in the LRT narrative, and Eigenpie is currently the best solution, and each LST has an independent The LRT doesn’t have to worry about making wedding clothes for other people. LST, which has a higher interest rate like mETH, can also continue to exert its advantages.

When can mstETH from Mint be traded on DEX? Will it be on Pendle?

It is obvious that the project party has great willingness and ability to promote these. Without others, these can bring huge bribery benefits to Magpie's subDAOs such as Cakepie and Penpie.

If you don’t understand Magpie’s architecture, you can refer to our previous tweets.

D. Earnings Expectation

In terms of income, let’s first look at the token economy:

IDO: 40%;

Airdrop: 10%;

Incentive 35%;

Magpie Treasury: 15% (not sold as usual, staking dividends to vlMGP);

is basically a FairLaunch operation. The difference is that most Fairlaunch whitelists currently have more default whitelists, while most of this IDO whitelists are explicit. To TVL providers.

The rights given to TVL providers are:

10% of the total airdrop;

60% of the IDO Share, IDO accounts for 40% of the total, $3M FDV valuation;

means that 10% of the total 60%*40% = 34% will be given to the TVL provider, This accounts for 34%/50% = ~70% of the initial circulation. There will be no VC selling pressure in the future.

The current LRT narrative is very hot. $RSTK with only $7M TVL has $35M mcap and $180M FDV. The valuations of several other projects have been released. Very high.

Eigenpie’s final TVL will most likely be much higher than RSTK. If benchmarked according to $RSTK’s FDV, the total profit of TVL providers can also reach: 10%*180 60%*40%*(180- 3) = $60M.

Assuming that the currency is issued two months later and the average TVL is $200M, it can also reach (60/2)/200*12= 180% APR. This does not include the income of the underlying Eigenlayer points. Participating as an early provider in the first 15 days will also result in a 2x points increase.

Let’s take a look at the previous increase of magpie’s subDAO IDO so far:

Penpie, IDO 3M FDV, 14 times

Radpie, two rounds of IDO average 7.5M FDV, 1.4 times

Cakepie, IDO 20M FDV, 2.4 times

This time to enter the LRT track with a larger market, not only did it take out 3M FDV, but the airdrops and IDO shares given to TVL providers were several times the PNP of the year. I wonder whether the income will return. moments and beyond.

Summary

Airdrops need to be grouped together to obtain greater growth;

The featured mechanism is ILRT to isolate the risks of each LST;

The advantage is that it can make full use of the Pendle/Pancake resources accumulated by Magpie to accelerate development;

Most of the rights and interests will be provided by TVL , Fairlaunch with transparent IDO quota.

The above is the detailed content of Eigenpie's airdrop gameplay, mechanism, prospects and revenue expectations. For more information, please follow other related articles on the PHP Chinese website!

Related articles

See more- What are the main characteristics of blockchain technology?

- Can blockchain only use Go language?

- How to use blockchain technology in Java to implement decentralized applications?

- Explore the intersection of JavaScript and blockchain technology

- Ripple is looking for a Cryptocurrency ETF Development Manager! Fox Reporter: XRP spot ETF will be launched first, followed by futures