Home >Backend Development >Python Tutorial >Summary of common methods for Python time series data manipulation

Summary of common methods for Python time series data manipulation

- WBOYWBOYWBOYWBOYWBOYWBOYWBOYWBOYWBOYWBOYWBOYWBOYWBforward

- 2023-04-24 22:22:062340browse

Time series data is a type of data collected over a period of time. It is often used in fields such as finance, economics, and meteorology, and is often analyzed to understand trends and patterns over time.

Pandas is a powerful and popular data manipulation library in Python, especially suitable for processing time series data. It provides a set of tools and functions to easily load, manipulate and analyze time series data.

In this article, we introduce indexing and slicing of time series data, resampling and rolling window calculations, and other useful common operations, which are key techniques for manipulating time series data using Pandas.

Data types

Python

In Python, there is no built-in data type specifically for representing dates. Under normal circumstances, the datetime object provided by the datetime module is used for date and time operations.

import datetime

t = datetime.datetime.now()

print(f"type: {type(t)} and t: {t}")

#type: <class 'datetime.datetime'> and t: 2022-12-26 14:20:51.278230Generally, we use strings to store dates and times. So we need to convert these strings into datetime objects when using them.

Generally, the time string has the following format:

- YYYY-MM-DD (e.g. 2022-01-01)

- YYYY/MM/DD (e.g. 2022/01/01)

- DD-MM-YYYY (e.g. 01-01-2022)

- DD/MM/YYYY (e.g. 01/01/2022)

- MM-DD-YYYY (e.g. 01-01-2022)

- MM/DD/YYYY (e.g. 01/01/2022)

- HH:MM:SS (e.g. 11:30 :00)

- HH:MM:SS AM/PM (e.g. 11:30:00 AM)

- HH:MM AM/PM (e.g. 11:30 AM)

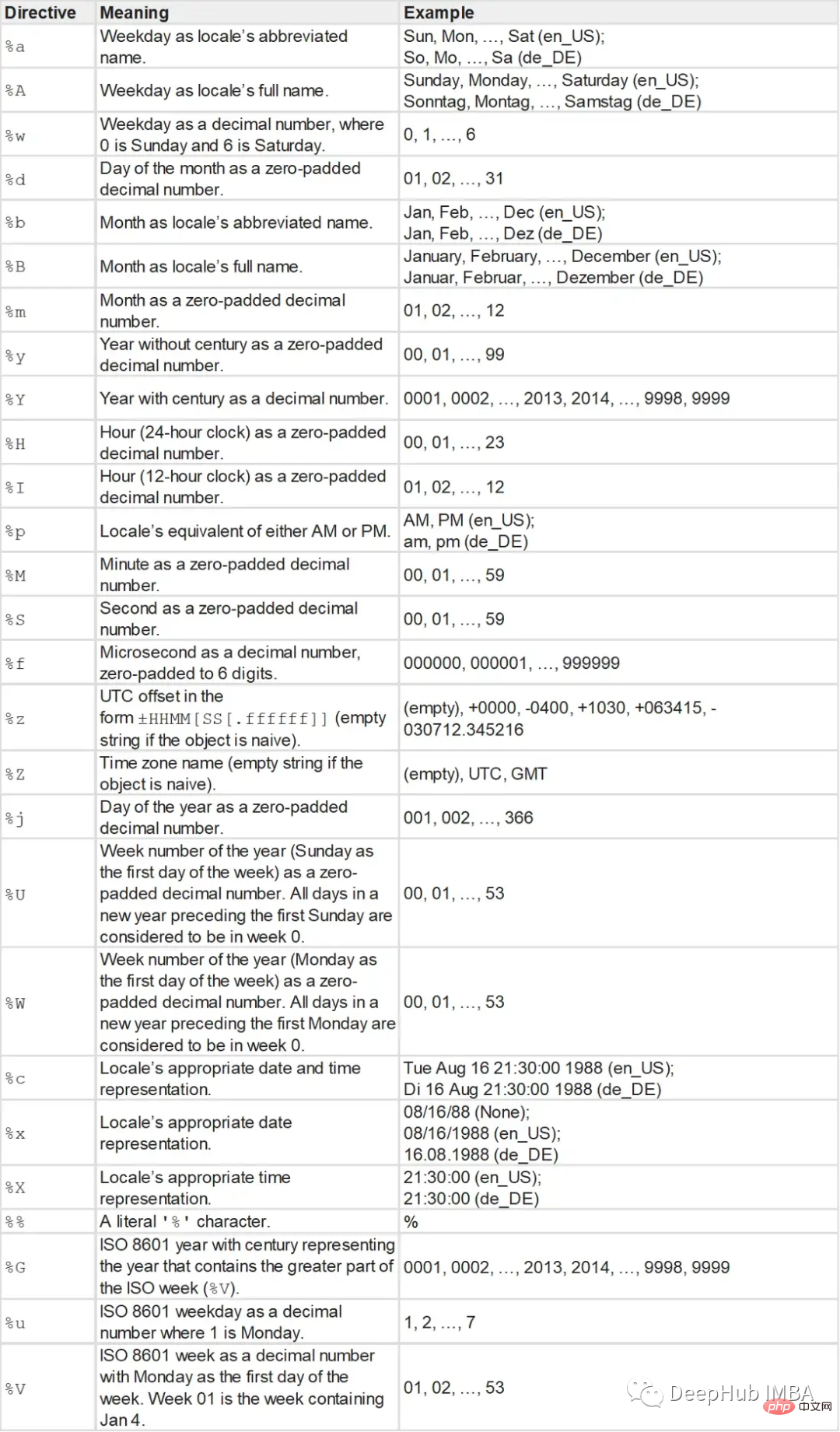

The strptime function takes a string and a format string as parameters and returns a datetime object.

string = '2022-01-01 11:30:09'

t = datetime.datetime.strptime(string, "%Y-%m-%d %H:%M:%S")

print(f"type: {type(t)} and t: {t}")

#type: <class 'datetime.datetime'> and t: 2022-01-01 11:30:09The format string is as follows:

You can also use the strftime function to convert the datetime object back to a string representation in a specific format.

t = datetime.datetime.now()

t_string = t.strftime("%m/%d/%Y, %H:%M:%S")

#12/26/2022, 14:38:47

t_string = t.strftime("%b/%d/%Y, %H:%M:%S")

#Dec/26/2022, 14:39:32Unix time (POSIX time or epoch time) is a system that represents time as a single numerical value. It represents the number of seconds elapsed since 00:00:00 Coordinated Universal Time (UTC) on Thursday, January 1, 1970.

Unix time and timestamp are often used interchangeably. Unix time is the standard version for creating timestamps. Generally use integer or floating point data types for storing timestamps and Unix times.

We can use the mktime method of the time module to convert datetime objects into Unix time integers. You can also use the fromtimestamp method of the datetime module.

#convert datetime to unix time import time from datetime import datetime t = datetime.now() unix_t = int(time.mktime(t.timetuple())) #1672055277 #convert unix time to datetime unix_t = 1672055277 t = datetime.fromtimestamp(unix_t) #2022-12-26 14:47:57

Use the dateutil module to parse the date string to obtain the datetime object.

from dateutil import parser

date = parser.parse("29th of October, 1923")

#datetime.datetime(1923, 10, 29, 0, 0)Pandas

Pandas provides three date data types:

1, Timestamp or DatetimeIndex: It functions like other index types, but also has functions for time Specialized functions for sequence operations.

t = pd.to_datetime("29/10/1923", dayfirst=True)

#Timestamp('1923-10-29 00:00:00')

t = pd.Timestamp('2019-01-01', tz = 'Europe/Berlin')

#Timestamp('2019-01-01 00:00:00+0100', tz='Europe/Berlin')

t = pd.to_datetime(["04/23/1920", "10/29/1923"])

#DatetimeIndex(['1920-04-23', '1923-10-29'], dtype='datetime64[ns]', freq=None)2. period or PeriodIndex: a time interval with a start and an end. It consists of fixed intervals.

t = pd.to_datetime(["04/23/1920", "10/29/1923"])

period = t.to_period("D")

#PeriodIndex(['1920-04-23', '1923-10-29'], dtype='period[D]')3. Timedelta or TimedeltaIndex: The time interval between two dates.

delta = pd.TimedeltaIndex(data =['1 days 03:00:00', '2 days 09:05:01.000030']) """ TimedeltaIndex(['1 days 02:00:00', '1 days 06:05:01.000030'], dtype='timedelta64[ns]', freq=None) """

In Pandas, you can use the to_datetime method to convert an object to datetime data type or do any other conversion.

import pandas as pd

df = pd.read_csv("dataset.txt")

df.head()

"""

date value

0 1991-07-01 3.526591

1 1991-08-01 3.180891

2 1991-09-01 3.252221

3 1991-10-01 3.611003

4 1991-11-01 3.565869

"""

df.info()

"""

<class 'pandas.core.frame.DataFrame'>

RangeIndex: 204 entries, 0 to 203

Data columns (total 2 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 date 204 non-null object

1 value 204 non-null float64

dtypes: float64(1), object(1)

memory usage: 3.3+ KB

"""

# Convert to datetime

df["date"] = pd.to_datetime(df["date"], format = "%Y-%m-%d")

df.info()

"""

<class 'pandas.core.frame.DataFrame'>

RangeIndex: 204 entries, 0 to 203

Data columns (total 2 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 date 204 non-null datetime64[ns]

1 value 204 non-null float64

dtypes: datetime64[ns](1), float64(1)

memory usage: 3.3 KB

"""

# Convert to Unix

df['unix_time'] = df['date'].apply(lambda x: x.timestamp())

df.head()

"""

date value unix_time

0 1991-07-01 3.526591 678326400.0

1 1991-08-01 3.180891 681004800.0

2 1991-09-01 3.252221 683683200.0

3 1991-10-01 3.611003 686275200.0

4 1991-11-01 3.565869 688953600.0

"""

df["date_converted_from_unix"] = pd.to_datetime(df["unix_time"], unit = "s")

df.head()

"""

date value unix_time date_converted_from_unix

0 1991-07-01 3.526591 678326400.0 1991-07-01

1 1991-08-01 3.180891 681004800.0 1991-08-01

2 1991-09-01 3.252221 683683200.0 1991-09-01

3 1991-10-01 3.611003 686275200.0 1991-10-01

4 1991-11-01 3.565869 688953600.0 1991-11-01

"""We can also use the parse_dates parameter to directly declare the date column when any file is loaded.

df = pd.read_csv("dataset.txt", parse_dates=["date"])

df.info()

"""

<class 'pandas.core.frame.DataFrame'>

RangeIndex: 204 entries, 0 to 203

Data columns (total 2 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 date 204 non-null datetime64[ns]

1 value 204 non-null float64

dtypes: datetime64[ns](1), float64(1)

memory usage: 3.3 KB

"""If it is a single time series data, it is best to use the date column as the index of the data set.

df.set_index("date",inplace=True)

"""

Value

date

1991-07-01 3.526591

1991-08-01 3.180891

1991-09-01 3.252221

1991-10-01 3.611003

1991-11-01 3.565869

... ...

2008-02-01 21.654285

2008-03-01 18.264945

2008-04-01 23.107677

2008-05-01 22.912510

2008-06-01 19.431740

"""Numpy also has its own datetime type np.Datetime64. Especially when working with large data sets, vectorization is very useful and should be used first.

import numpy as np

arr_date = np.array('2000-01-01', dtype=np.datetime64)

arr_date

#array('2000-01-01', dtype='datetime64[D]')

#broadcasting

arr_date = arr_date + np.arange(30)

"""

array(['2000-01-01', '2000-01-02', '2000-01-03', '2000-01-04',

'2000-01-05', '2000-01-06', '2000-01-07', '2000-01-08',

'2000-01-09', '2000-01-10', '2000-01-11', '2000-01-12',

'2000-01-13', '2000-01-14', '2000-01-15', '2000-01-16',

'2000-01-17', '2000-01-18', '2000-01-19', '2000-01-20',

'2000-01-21', '2000-01-22', '2000-01-23', '2000-01-24',

'2000-01-25', '2000-01-26', '2000-01-27', '2000-01-28',

'2000-01-29', '2000-01-30'], dtype='datetime64[D]')

"""Useful functions

Listed below are some functions that may be useful for time series.

df = pd.read_csv("dataset.txt", parse_dates=["date"])

df["date"].dt.day_name()

"""

0 Monday

1 Thursday

2 Sunday

3 Tuesday

4 Friday

...

199 Friday

200 Saturday

201 Tuesday

202 Thursday

203 Sunday

Name: date, Length: 204, dtype: object

"""DataReader

Pandas_datareader is an auxiliary library for the pandas library. It provides many common financial time series data.

#pip install pandas-datareader from pandas_datareader import wb #GDP per Capita From World Bank df = wb.download(indicator='NY.GDP.PCAP.KD', country=['US', 'FR', 'GB', 'DK', 'NO'], start=1960, end=2019) """ NY.GDP.PCAP.KD country year Denmark 2019 57203.027794 2018 56563.488473 2017 55735.764901 2016 54556.068955 2015 53254.856370 ... ... United States 1964 21599.818705 1963 20701.269947 1962 20116.235124 1961 19253.547329 1960 19135.268182 [300 rows x 1 columns] """

Date range

We can use the date_range method of pandas to define a date range.

pd.date_range(start="2021-01-01", end="2022-01-01", freq="D")

"""

DatetimeIndex(['2021-01-01', '2021-01-02', '2021-01-03', '2021-01-04',

'2021-01-05', '2021-01-06', '2021-01-07', '2021-01-08',

'2021-01-09', '2021-01-10',

...

'2021-12-23', '2021-12-24', '2021-12-25', '2021-12-26',

'2021-12-27', '2021-12-28', '2021-12-29', '2021-12-30',

'2021-12-31', '2022-01-01'],

dtype='datetime64[ns]', length=366, freq='D')

"""

pd.date_range(start="2021-01-01", end="2022-01-01", freq="BM")

"""

DatetimeIndex(['2021-01-29', '2021-02-26', '2021-03-31', '2021-04-30',

'2021-05-31', '2021-06-30', '2021-07-30', '2021-08-31',

'2021-09-30', '2021-10-29', '2021-11-30', '2021-12-31'],

dtype='datetime64[ns]', freq='BM')

"""

fridays= pd.date_range('2022-11-01', '2022-12-31', freq="W-FRI")

"""

DatetimeIndex(['2022-11-04', '2022-11-11', '2022-11-18', '2022-11-25',

'2022-12-02', '2022-12-09', '2022-12-16', '2022-12-23',

'2022-12-30'],

dtype='datetime64[ns]', freq='W-FRI')

"""

We can create a time series using the timedelta_range method.

t = pd.timedelta_range(0, periods=10, freq="H") """ TimedeltaIndex(['0 days 00:00:00', '0 days 01:00:00', '0 days 02:00:00', '0 days 03:00:00', '0 days 04:00:00', '0 days 05:00:00', '0 days 06:00:00', '0 days 07:00:00', '0 days 08:00:00', '0 days 09:00:00'], dtype='timedelta64[ns]', freq='H') """

Formatting

Our dt.strftime method changes the format of the date column.

df["new_date"] = df["date"].dt.strftime("%b %d, %Y")

df.head()

"""

date value new_date

0 1991-07-01 3.526591 Jul 01, 1991

1 1991-08-01 3.180891 Aug 01, 1991

2 1991-09-01 3.252221 Sep 01, 1991

3 1991-10-01 3.611003 Oct 01, 1991

4 1991-11-01 3.565869 Nov 01, 1991

"""Parsing

Parses the datetime object and obtains the child object of the date.

df["year"] = df["date"].dt.year df["month"] = df["date"].dt.month df["day"] = df["date"].dt.day df["calendar"] = df["date"].dt.date df["hour"] = df["date"].dt.time df.head() """ date value year month day calendar hour 0 1991-07-01 3.526591 1991 7 1 1991-07-01 00:00:00 1 1991-08-01 3.180891 1991 8 1 1991-08-01 00:00:00 2 1991-09-01 3.252221 1991 9 1 1991-09-01 00:00:00 3 1991-10-01 3.611003 1991 10 1 1991-10-01 00:00:00 4 1991-11-01 3.565869 1991 11 1 1991-11-01 00:00:00 """

You can also recombine them.

df["date_joined"] = pd.to_datetime(df[["year","month","day"]]) print(df["date_joined"]) """ 0 1991-07-01 1 1991-08-01 2 1991-09-01 3 1991-10-01 4 1991-11-01 ... 199 2008-02-01 200 2008-03-01 201 2008-04-01 202 2008-05-01 203 2008-06-01 Name: date_joined, Length: 204, dtype: datetime64[ns]

Filter query

Use the loc method to filter the DataFrame.

df = df.loc["2021-01-01":"2021-01-10"]

truncate can query data in two time intervals

df_truncated = df.truncate('2021-01-05', '2022-01-10')

Common data operations

The following is to perform operations on the values in the time series data set. We use the yfinance library to create a stock dataset for our example.

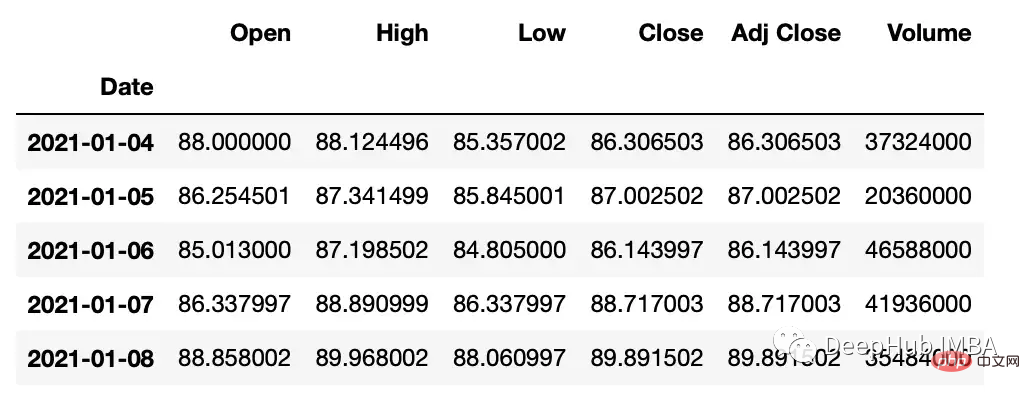

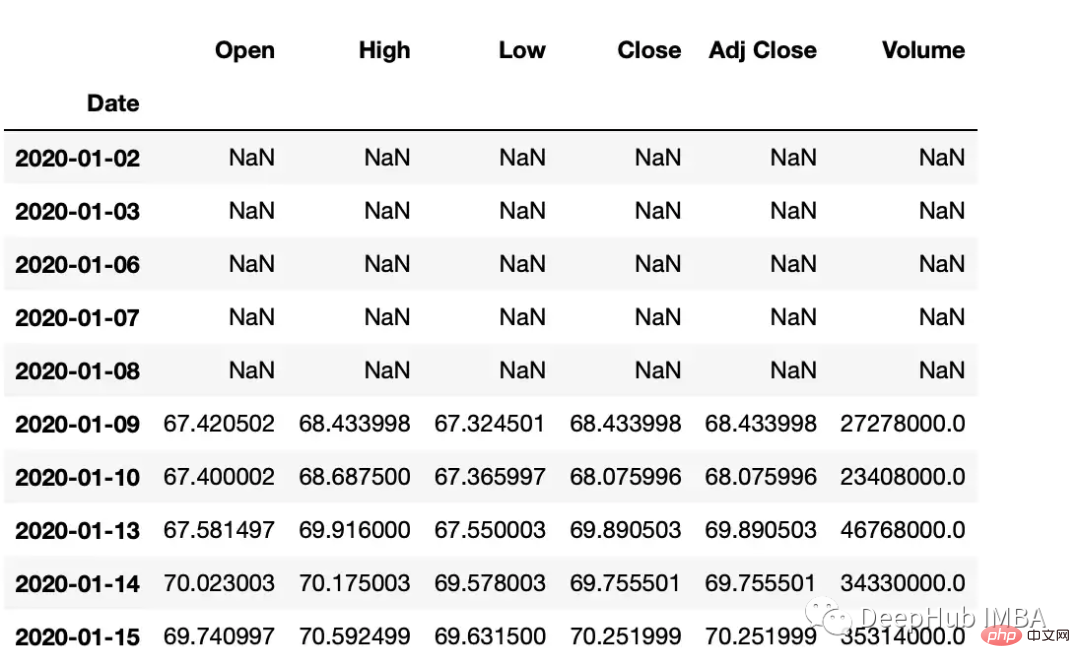

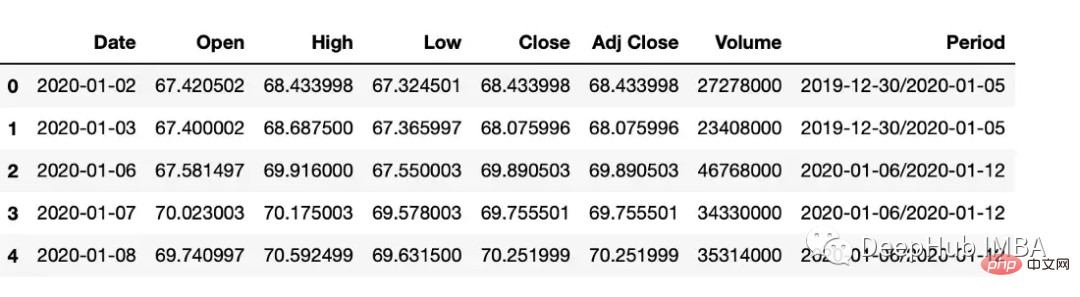

#get google stock price data import yfinance as yf start_date = '2020-01-01' end_date = '2023-01-01' ticker = 'GOOGL' df = yf.download(ticker, start_date, end_date) df.head() """ Date Open High Low Close Adj Close Volume 2020-01-02 67.420502 68.433998 67.324501 68.433998 68.433998 27278000 2020-01-03 67.400002 68.687500 67.365997 68.075996 68.075996 23408000 2020-01-06 67.581497 69.916000 67.550003 69.890503 69.890503 46768000 2020-01-07 70.023003 70.175003 69.578003 69.755501 69.755501 34330000 2020-01-08 69.740997 70.592499 69.631500 70.251999 70.251999 35314000 """

Calculate difference

The diff function can calculate the interpolation between one element and another element.

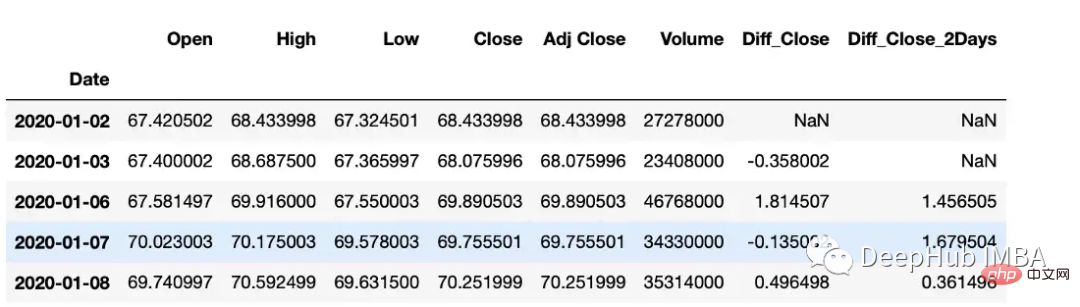

#subtract that day's value from the previous day df["Diff_Close"] = df["Close"].diff() #Subtract that day's value from the day's value 2 days ago df["Diff_Close_2Days"] = df["Close"].diff(periods=2)

累计总数

df["Volume_Cumulative"] = df["Volume"].cumsum()

滚动窗口计算

滚动窗口计算(移动平均线)。

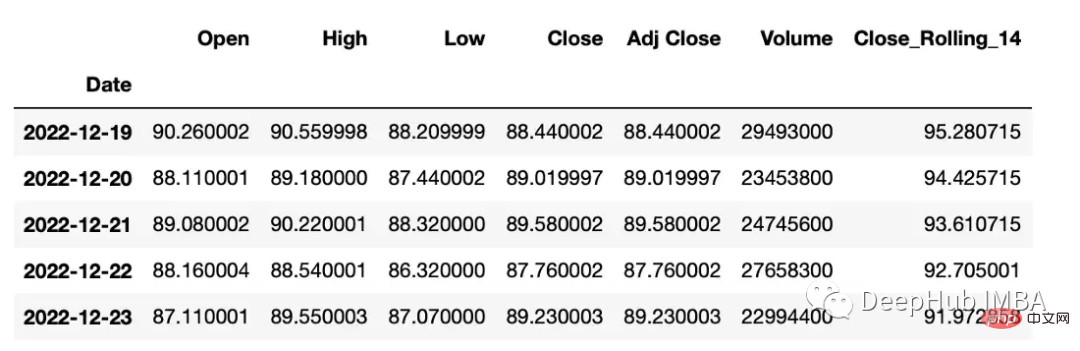

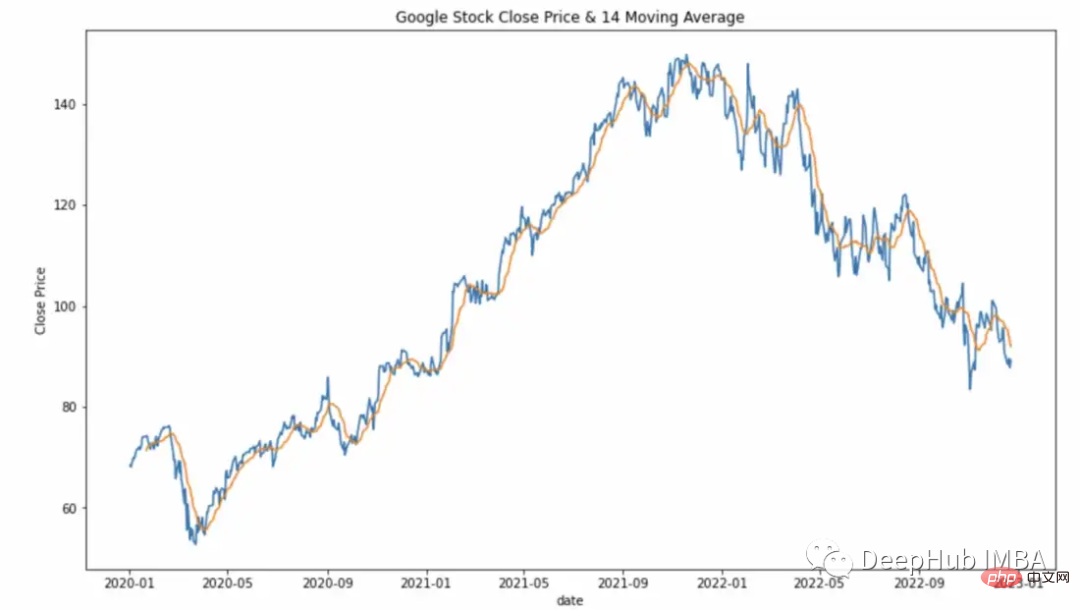

df["Close_Rolling_14"] = df["Close"].rolling(14).mean() df.tail()

可以对我们计算的移动平均线进行可视化

常用的参数:

- center:决定滚动窗口是否应以当前观测值为中心。

- min_periods:窗口中产生结果所需的最小观测次数。

s = pd.Series([1, 2, 3, 4, 5]) #the rolling window will be centered on each observation rolling_mean = s.rolling(window=3, center=True).mean() """ 0 NaN 1 2.0 2 3.0 3 4.0 4 NaN dtype: float64 Explanation: first window: [na 1 2] = na second window: [1 2 3] = 2 """ # the rolling window will not be centered, #and will instead be anchored to the left side of the window rolling_mean = s.rolling(window=3, center=False).mean() """ 0 NaN 1 NaN 2 2.0 3 3.0 4 4.0 dtype: float64 Explanation: first window: [na na 1] = na second window: [na 1 2] = na third window: [1 2 3] = 2 """

平移

Pandas有两个方法,shift()和tshift(),它们可以指定倍数移动数据或时间序列的索引。Shift()移位数据,而tshift()移位索引。

#shift the data df_shifted = df.shift(5,axis=0) df_shifted.head(10) #shift the indexes df_tshifted = df.tshift(periods = 4, freq = 'D') df_tshifted.head(10)

df_shifted

df_tshifted

时间间隔转换

在 Pandas 中,操 to_period 函数允许将日期转换为特定的时间间隔。可以获取具有许多不同间隔或周期的日期

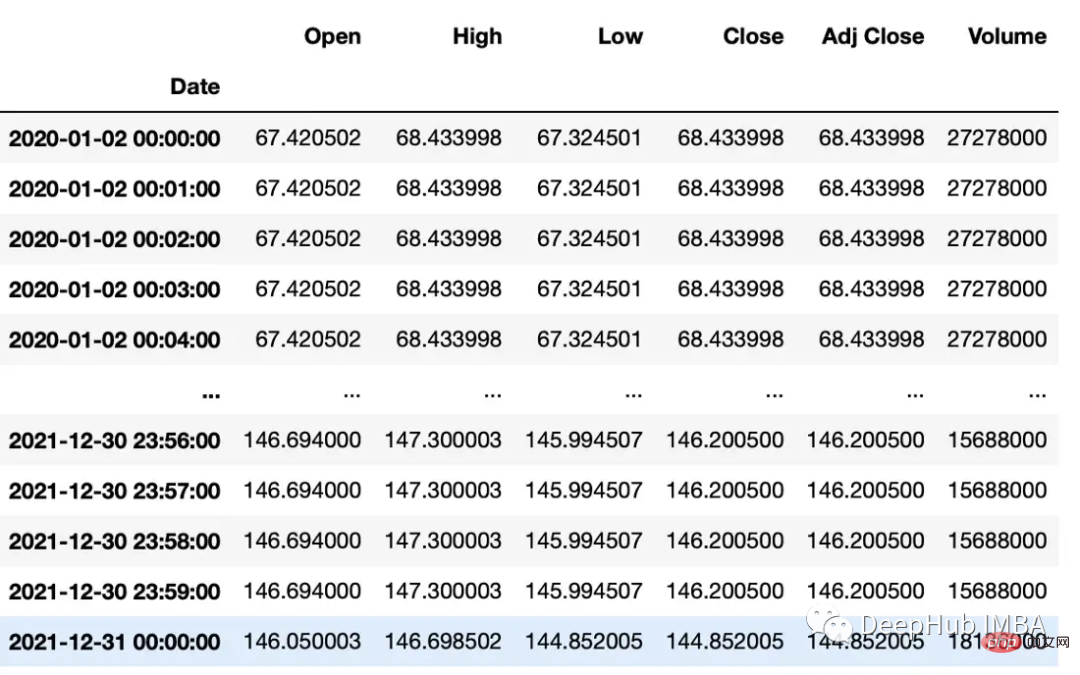

df["Period"] = df["Date"].dt.to_period('W')

频率

Asfreq方法用于将时间序列转换为指定的频率。

monthly_data = df.asfreq('M', method='ffill')

常用参数:

freq:数据应该转换到的频率。这可以使用字符串别名(例如,'M'表示月,'H'表示小时)或pandas偏移量对象来指定。

method:如何在转换频率时填充缺失值。这可以是'ffill'(向前填充)或'bfill'(向后填充)之类的字符串。

采样

resample可以改变时间序列频率并重新采样。我们可以进行上采样(到更高的频率)或下采样(到更低的频率)。因为我们正在改变频率,所以我们需要使用一个聚合函数(比如均值、最大值等)。

resample方法的参数:

rule:数据重新采样的频率。这可以使用字符串别名(例如,'M'表示月,'H'表示小时)或pandas偏移量对象来指定。

#down sample

monthly_data = df.resample('M').mean()

#up sample

minute_data = data.resample('T').ffill()

百分比变化

使用pct_change方法来计算日期之间的变化百分比。

df["PCT"] = df["Close"].pct_change(periods=2) print(df["PCT"]) """ Date 2020-01-02 NaN 2020-01-03 NaN 2020-01-06 0.021283 2020-01-07 0.024671 2020-01-08 0.005172 ... 2022-12-19 -0.026634 2022-12-20 -0.013738 2022-12-21 0.012890 2022-12-22 -0.014154 2022-12-23 -0.003907 Name: PCT, Length: 752, dtype: float64 """

总结

在Pandas和NumPy等库的帮助下,可以对时间序列数据执行广泛的操作,包括过滤、聚合和转换。本文介绍的是一些在工作中经常遇到的常见操作,希望对你有所帮助。

The above is the detailed content of Summary of common methods for Python time series data manipulation. For more information, please follow other related articles on the PHP Chinese website!