The Fat Wallet Thesis

The "Fat Wallet" thesis argues that as protocols and applications continue to "thin out," individuals who possess the two most valuable resources—distribution and order flow—will gain more space.

The cryptocurrency ecosystem is a complex and ever-evolving landscape. As the industry matures, there is a growing debate about how value will ultimately be distributed among the various layers of the ecosystem.

Historically, the focus has been on protocols versus applications. However, a third layer that has been largely overlooked is wallets. In this article, we will explore the "Fat Wallet Thesis," which argues that wallets will gradually come to dominate the blockchain ecosystem as they control the critical user entry points and transaction flows.

As the roles of underlying protocols and applications diminish, we will examine how wallets can capitalize on their proximity to end users by charging fees for order flow and offering promotional services for application distribution. Finally, we will discuss why two alternative front ends—Jupiter and Infinex—may ultimately outcompete wallets in the race to capture user attention and transaction orders.

Throughout the history of cryptocurrency development, discussions about how value will ultimately accumulate within the blockchain ecosystem have been ongoing. Although historical core debates have primarily focused on protocols versus applications, there is a third layer in this ecosystem that has been overlooked—wallets.

The "Fat Wallet" thesis posits that as protocols and applications continue to "thin out," individuals who possess the two most valuable resources—distribution and order flow—will gain more space. Moreover, as the ultimate front end, I believe no one is better positioned than wallets to monetize this value.

This article aims to achieve three objectives: first, to outline three structural trends that will continue to commoditize the protocol and application layers. Second, we will explore various ways wallets can monetize their proximity to end users, including Payment-for-Order-Flow (PFOF) and selling application distribution as a service (DaaS).

Finally, we will discuss why two alternative front ends—Jupiter and Infinex—may ultimately outperform wallets in the competition for end users.

If a product in this layer increases its commission rate, will users turn to cheaper alternatives?

In other words, if Arbitrum raises its commission rate, will users switch to other protocols like Base, and vice versa? Similarly, at the application layer, if dYdX raises its commission rate, will users turn to the nth undifferentiated perpetual contract decentralized exchange (DEX)?

Based on this logic, we can identify where the switching costs are highest, and thus who possesses asymmetric pricing power. Similarly, we can use this framework to identify which layer will become increasingly commoditized over time.

While historically protocols have had disproportionate pricing power, I believe this phenomenon is changing. Currently, there are three structural trends that are continuously "thinning" the protocol layer:

1. Multi-chain Applications and Chain Abstraction: As multi-chain becomes a fundamental requirement for applications to remain competitive, cross-blockchain user experiences will become increasingly indistinguishable, thereby lowering the switching costs at the protocol layer. Additionally, through abstracted bridging, chain abstraction will further compress switching costs. Thus, applications will no longer rely on the network effects of a single chain but will increasingly depend on front-end distribution.

2. Maturity of the MEV Supply Chain: While MEV will not be completely eliminated, many initiatives at the application layer and closer to the base layer will continuously redistribute the amount of MEV extracted from end users. As the MEV supply chain matures, value will increasingly ascend to the upstream of the MEV supply chain and asymmetrically accumulate in the hands of those with the most unique user order flows. This means protocols will lose bargaining power, thereby "thinning out," while front ends and wallets will gain leverage, thus "thickening."

3. Development Towards an Agency Paradigm: In a world where transactions are primarily executed by agents and "solvers" rather than humans, attracting this agency flow will become key to survival in blockchain. Importantly, given that agents and "solvers" are programmed to primarily optimize for best execution, protocols will no longer compete on intangible factors like "vibe" and "alignment." Instead, transaction fees and liquidity will be the only important factors—this will further "thin" the protocol layer as protocols are forced to compress fees and incentivize liquidity to remain competitive.

Thus, revisiting our initial question—if protocols raise their commission rates, will users switch to cheaper alternatives?—while it may not be obvious today, I believe the answer will increasingly be "yes," as switching costs continue to compress.

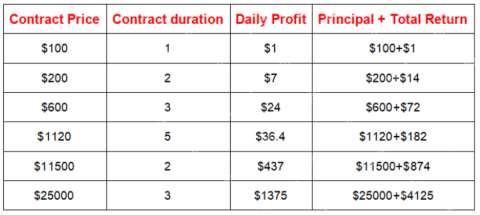

Data Source: Dune Analytics @0xKofi

Intuitively, one might assume that if protocols become "thinner," applications must inevitably become "thicker." While this value will certainly be recaptured by certain applications, the "Thick Application Theory" alone is simplistic. Different applications in vertical domains accumulate value in various ways. Therefore, the question should not be—"Will applications become thicker?"—but rather—"Which specific applications?"

As I outlined in “Identifying New Frameworks for Crypto Market Moats”, the unique structural differences of crypto applications—forkability, composability, and token-based acquisition—have a net effect of lowering barriers

The above is the detailed content of The Fat Wallet Thesis. For more information, please follow other related articles on the PHP Chinese website!

FloppyPepe (FPPE) Price Could Explode As Bitcoin (BTC) Price Rallies Towards $450,000May 09, 2025 am 11:54 AM

FloppyPepe (FPPE) Price Could Explode As Bitcoin (BTC) Price Rallies Towards $450,000May 09, 2025 am 11:54 AMAccording to a leading finance CEO, the Bitcoin price could be set for a move to $450,000. This Bitcoin price projection comes after a resurgence of good performances, signaling that the bear market may end.

Pi Network Confirms May 14 Launch—Qubetics and OKB Surge as Best Cryptos to Join for Long Term in 2025May 09, 2025 am 11:52 AM

Pi Network Confirms May 14 Launch—Qubetics and OKB Surge as Best Cryptos to Join for Long Term in 2025May 09, 2025 am 11:52 AMExplore why Qubetics, Pi Network, and OKB rank among the Best Cryptos to Join for Long Term. Get updated presale stats, features, and key real-world use cases.

Sun Life Financial Inc. (TSX: SLF) (NYSE: SLF) Declares a Dividend of $0.88 Per ShareMay 09, 2025 am 11:50 AM

Sun Life Financial Inc. (TSX: SLF) (NYSE: SLF) Declares a Dividend of $0.88 Per ShareMay 09, 2025 am 11:50 AMTORONTO, May 8, 2025 /CNW/ - The Board of Directors (the "Board") of Sun Life Financial Inc. (the "Company") (TSX: SLF) (NYSE: SLF) today announced that a dividend of $0.88 per share on the common shares of the Company has been de

Sun Life Announces Intended Renewal of Normal Course Issuer BidMay 09, 2025 am 11:48 AM

Sun Life Announces Intended Renewal of Normal Course Issuer BidMay 09, 2025 am 11:48 AMMay 7, 2025, the Company had purchased on the TSX, other Canadian stock exchanges and/or alternative Canadian trading platforms

The Bitcoin price has hit $100k for the first time since February, trading at $101.3k at press time.May 09, 2025 am 11:46 AM

The Bitcoin price has hit $100k for the first time since February, trading at $101.3k at press time.May 09, 2025 am 11:46 AMBTC's strong correlation with the Global M2 money supply is playing out once again, with the largest cryptocurrency now poised for new all-time highs.

Coinbase (COIN) Q1 CY2025 Highlights: Revenue Falls Short of Expectations, but Sales Rose 24.2% YoY to $2.03BMay 09, 2025 am 11:44 AM

Coinbase (COIN) Q1 CY2025 Highlights: Revenue Falls Short of Expectations, but Sales Rose 24.2% YoY to $2.03BMay 09, 2025 am 11:44 AMBlockchain infrastructure company Coinbase (NASDAQ: COIN) fell short of the market’s revenue expectations in Q1 CY2025, but sales rose 24.2% year

Ripple Labs and the SEC Have Officially Reached a Settlement AgreementMay 09, 2025 am 11:42 AM

Ripple Labs and the SEC Have Officially Reached a Settlement AgreementMay 09, 2025 am 11:42 AMRipple Labs and the U.S. Securities and Exchange Commission (SEC) have officially reached a deal that, if approved by a judge, will bring their years-long legal battle to a close.

JA Mining Helps Global Users Share the Benefits of the Bitcoin Bull MarketMay 09, 2025 am 11:40 AM

JA Mining Helps Global Users Share the Benefits of the Bitcoin Bull MarketMay 09, 2025 am 11:40 AMBy lowering the threshold for mining and providing compliance protection, JA Mining helps global users share the benefits of the Bitcoin bull market.

Hot AI Tools

Undresser.AI Undress

AI-powered app for creating realistic nude photos

AI Clothes Remover

Online AI tool for removing clothes from photos.

Undress AI Tool

Undress images for free

Clothoff.io

AI clothes remover

Video Face Swap

Swap faces in any video effortlessly with our completely free AI face swap tool!

Hot Article

Hot Tools

SublimeText3 Chinese version

Chinese version, very easy to use

WebStorm Mac version

Useful JavaScript development tools

EditPlus Chinese cracked version

Small size, syntax highlighting, does not support code prompt function

DVWA

Damn Vulnerable Web App (DVWA) is a PHP/MySQL web application that is very vulnerable. Its main goals are to be an aid for security professionals to test their skills and tools in a legal environment, to help web developers better understand the process of securing web applications, and to help teachers/students teach/learn in a classroom environment Web application security. The goal of DVWA is to practice some of the most common web vulnerabilities through a simple and straightforward interface, with varying degrees of difficulty. Please note that this software

Zend Studio 13.0.1

Powerful PHP integrated development environment